Every company registered under the Companies Act, 2013 must carefully examine whether it is required to file Form DPT-3 with the Registrar of Companies (ROC). Even companies that have not accepted public deposits may still be required to file DPT-3 for reporting outstanding loans or money received which is not treated as deposits.

Many companies ignore this compliance assuming that DPT-3 is applicable only to companies accepting deposits from the public. However, the scope of Form DPT-3 is much wider and covers several outstanding amounts including unsecured loans from directors, advances from customers, and inter-corporate borrowings.

In this article, a complete guide on Form DPT-3 Filing for FY 2025-26 is explained including applicability, exemptions, due date, reporting requirements, attachments, penalties, and the step-by-step filing process.

What is Form DPT-3?

Form DPT-3 is a ROC e-form prescribed under Rule 16 and Rule 16A of the Companies (Acceptance of Deposits) Rules, 2014.

The form is used by companies to furnish details of:

- Deposits accepted by the company; and/or

- Outstanding receipt of money or loan not considered as deposits.

The form is filed annually with the Registrar of Companies (ROC).

Purpose of Filing Form DPT-3

The Ministry of Corporate Affairs (MCA) introduced DPT-3 to monitor:

- Outstanding loans and borrowings of companies

- Acceptance of deposits by companies

- Financial liabilities not treated as deposits

Compliance with deposit-related provisions under the Companies Act, 2013

Form DPT-3 Filing Due Date for FY 2025-26

The annual return in Form DPT-3 for FY 2025-26 is generally required to be filed on or before:

30 June 2026

The details are required to be reported as on:

31 March 2026

Companies should avoid last-minute filing due to MCA portal congestion and DSC-related issues.

The Ministry of Corporate Affairs has issued General Circular No. 02/2026 for granting relaxation in paying additional fees in case of delay in filing Form DPT-3 for the financial year ending on 31 March 2026 up to 31 July 2026.

Who is Required to File Form DPT-3?

Form DPT-3 is applicable to all companies except specifically exempted entities.

The following companies are generally required to examine applicability and file DPT-3 if applicable:

- Private Limited Companies

- Public Limited Companies

- One Person Companies (OPC)

- Small Companies

- Section 8 Companies

- Subsidiary Companies

- Associate Companies

Even if a company has not accepted public deposits, it may still need to file DPT-3 for reporting exempted outstanding amounts.

Which Amounts are Reportable in DPT-3?

The following outstanding amounts are commonly reportable in Form DPT-3 if outstanding as on 31 March 2026:

| Nature of Amount | Generally Reportable |

|---|---|

| Unsecured loan from directors | Yes |

| Loan from shareholders | Yes |

| Inter-corporate borrowings | Yes |

| Security deposits from customers/employees | Yes |

| Advance from customers | Yes |

| Share application money pending allotment | Yes |

| Loan from holding company | Yes |

| Commercial borrowings | Yes |

| Outstanding expenses/creditors | Depending on nature |

Amounts Not Treated as Deposits under Companies Act

Certain amounts are specifically excluded from the definition of “deposit” under Rule 2(1)(c) of the Companies (Acceptance of Deposits) Rules, 2014.

Common examples include:

- Loan from directors (subject to declaration conditions)

- Inter-corporate loans

- Secured borrowings from banks

- Share application money received within prescribed time

- Business advances received in ordinary course of business

- Amount received from Government

Although these may not be treated as deposits, they may still require reporting in DPT-3.

Which companies are exempt from filing DPT-3?

The following entities are generally exempt from DPT-3 requirements:

- Banking Companies

- Non-Banking Financial Companies (NBFCs)

- Housing Finance Companies

- Government Companies (subject to applicable exemptions)

However, companies should examine specific legal provisions and notifications before concluding exemption.

Is DPT-3 mandatory for Private Limited Companies?

Yes. In many cases, private limited companies are required to file DPT-3 even if they have only exempted loans or advances.

For example:

- Director’s unsecured loan outstanding

- Loan from relatives of directors

- Inter-corporate loan

- Customer advances

Therefore, most private limited companies should review applicability every financial year.

Is Nil DPT-3 Filing Mandatory?

The Companies Act and Rules do not expressly mandate filing of Nil DPT-3 in every case.

However, professional practice may differ depending upon the company’s financial position and outstanding transactions.

If no reportable outstanding amount exists as on 31 March 2026, professional advice should be taken regarding filing requirements.

Documents Required for Filing Form DPT-3

The following documents/details are generally required:

- Auditor’s Certificate

- Details of outstanding money/loan

- Net worth details

- Credit rating details, if applicable

- Copy of trust deed, if applicable

- Board Resolution, if required

- CIN and company master data

Auditor’s Certificate in DPT-3

Depending upon the nature of filing and purpose selected in Form DPT-3, attachment requirements may vary. In practice, companies generally attach an Auditor’s Certificate certifying the outstanding amounts reported in the form Total outstanding amounts

The certificate should be obtained before filing the form.

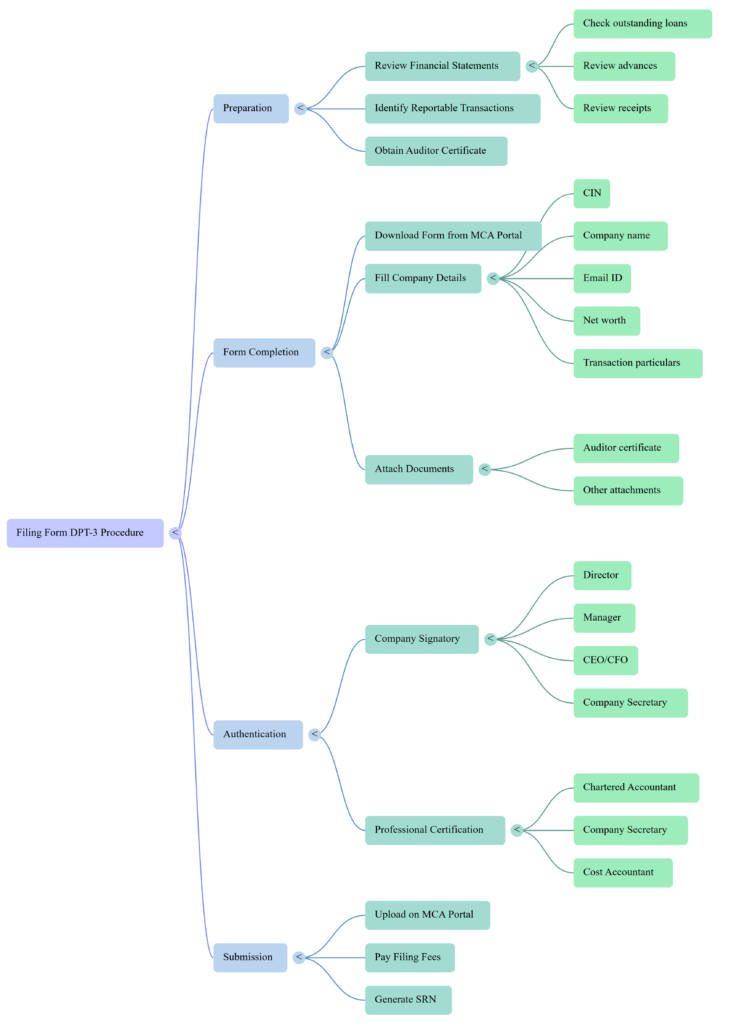

Step-by-Step Procedure for Filing Form DPT-3

Step 1: Review Financial Statements

Check all outstanding loans, advances, and receipts as on 31 March 2026.

Step 2: Identify Reportable Transactions

Determine which outstanding amounts are required to be reported in DPT-3.

Step 3: Obtain Auditor Certificate

Get the Auditor’s Certificate prepared and signed, if required.

Step 4: Download Form DPT-3

Download the latest version of Form DPT-3 from MCA portal.

Step 5: Fill Company Details

Enter:

- CIN

- Company name

- Email ID

- Net worth

- Particulars of outstanding transactions

Step 6: Attach Supporting Documents

Attach:

- Auditor certificate

- Other required attachments

Step 7: Affix DSC

The form must be digitally signed by:

- Director/Manager/CEO/CFO/Company Secretary

Professional certification by (if applicable):

- Chartered Accountant

- Company Secretary

- Cost Accountant

is also required.

Step 8: Upload Form on MCA Portal

Upload the form and pay prescribed filing fees.

Step 9: Generate SRN

After successful submission, SRN is generated for future reference.

Filing Fees for Form DPT-3

The filing fees depend upon the nominal share capital of the company as prescribed under Companies (Registration Offices and Fees) Rules.

Additional fees may apply for delayed filing.

Penalty for Non-Filing of DPT-3

Non-filing or delayed filing of DPT-3 may lead to:

- Additional filing fees

- ROC notices

- Adjudication proceedings

- Penalty under Companies Act, 2013

- Compliance qualification during due diligence or audits

Timely filing helps maintain proper compliance status of the company.

Important Practical Points for DPT-3 Filing

- Review director loan declarations properly.

- Verify whether customer advances have become overdue.

- Cross-check figures with audited financial statements.

- Ensure consistency with balance sheet disclosures.

Avoid incorrect classification of deposits and exempted borrowings.

Conclusion

Form DPT-3 is an important annual ROC compliance which should not be ignored merely because the company has not accepted public deposits. The reporting requirements under DPT-3 cover several categories of outstanding loans and exempted transactions.

Companies should carefully examine their financial statements, identify reportable amounts, obtain auditor certification, and complete filing within the prescribed due date to avoid penalties and compliance issues.

To know about the annual compliances applicable upon Private Limited Company. Read our Article on Annual Compliance for Private Limited Company in India (2026) – Complete Checklist, Due Dates

Need Assistance in DPT-3 Filing?

For professional assistance in:

- DPT-3 Filing

- ROC Annual Compliance

- Company Law Advisory

- Drafting & Certification

- MCA Filings

Contact Legnex Solutions for expert support.

Frequently Asked Questions (FAQs)

What is the due date of DPT-3 for FY 2025-26?

The due date is generally 30 June 2026 for reporting outstanding amounts as on 31 March 2026.

Is DPT-3 mandatory for private limited companies?

Yes, many private limited companies are required to file DPT-3 even if they have exempted loans only.

Is auditor certificate mandatory for DPT-3?

In many practical cases, companies attach an Auditor’s Certificate while filing Form DPT-3. However, attachment requirements may vary depending upon the nature of filing and applicable MCA requirements.

Are director loans reportable in DPT-3?

Yes, unsecured loans from directors are generally reportable if outstanding as on 31 March 2026.

Is DPT-3 applicable if there is no deposit?

Yes. DPT-3 may still apply for reporting transactions not treated as deposits.

Are customer advances reportable in DPT-3?

In many cases, yes. The nature and period of advance should be examined carefully.